When Indian households turn to family gold in times of need, they draw on a familiar instinct: gold is not just jewellery, it is ready cash. For Muthoot Finance, this instinct is the foundation of a business that has transformed cultural tradition into a financial powerhouse. The recent rally in gold prices didn’t create this model; it only amplified it, boosting balance sheets, increasing loan sizes, and lifting margins and earnings.

A family trade business becomes a national machine

Muthoot’s story is instructive for understanding why gold loans work at scale. The group traces its roots to Kerala in the late nineteenth century, evolving from trading activities into financial intermediation and, by the early 1970s, into gold-backed lending. That origin explains two persistent features: cultural affinity with customers in smaller towns and a branch-first distribution philosophy. The brand’s red kiosks are access nodes where valuation, custody, and relationship intersect.

The transaction that repeats a million times

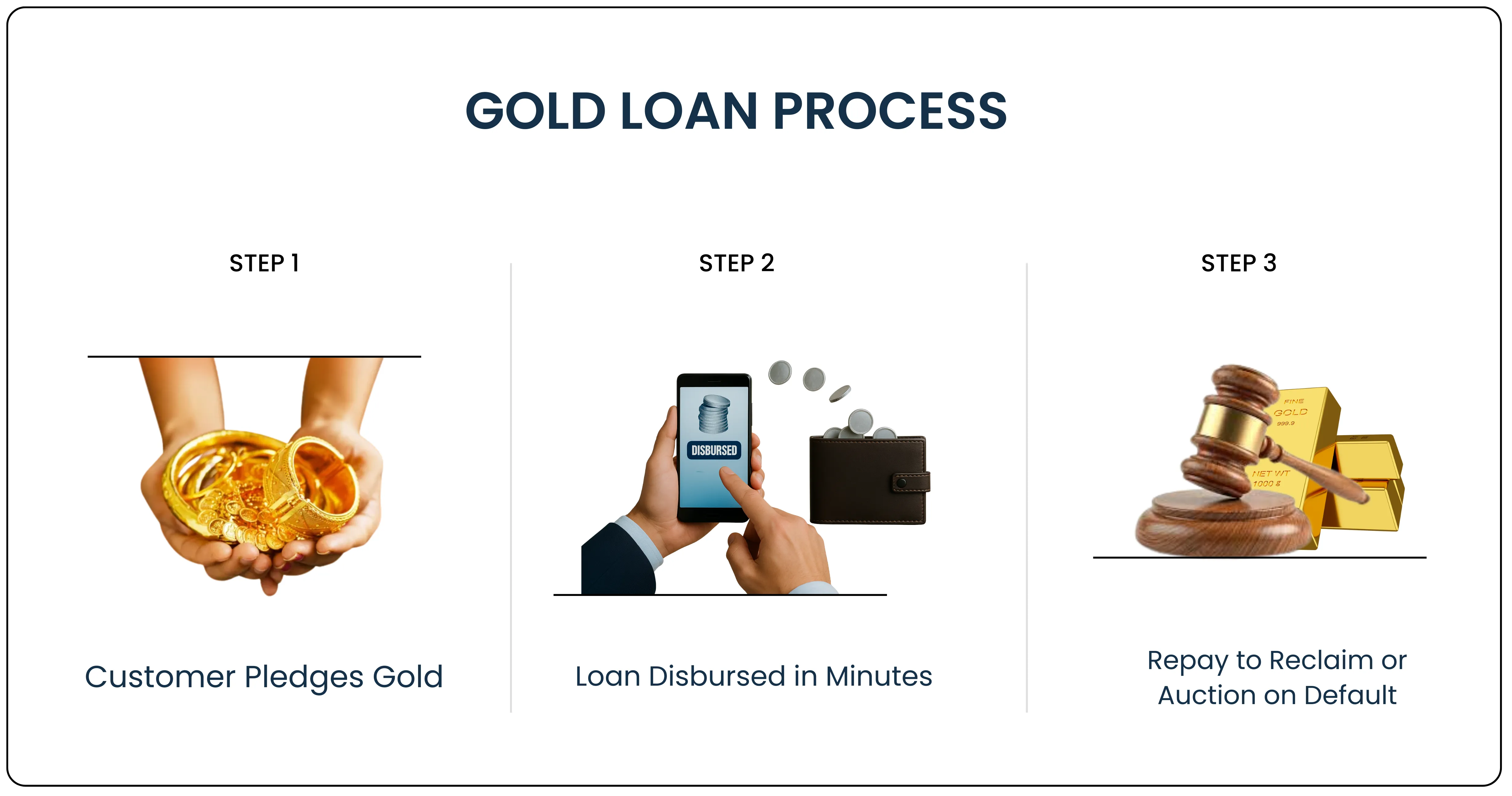

At its core, Muthoot’s model is straightforward: customers pledge jewellery, the branch verifies purity and weight, and a loan is given based on a Loan-to-Value percentage of the market price. Repay the loan, and the jewellery is returned; default, and it goes to a regulated auction.

The beauty lies in its repeatability rather than complexity, minimal paperwork, instant disbursal, and a lifeline for households in need without forcing the sale of assets.

Also Read: Decoding Rapido’s Entry into Food Delivery with ‘OWNLY’

Economics and scale

Revenue comes from interest income along with ancillary charges such as processing fees, handling costs, and late-payment penalties. Typical retail yields range between 12% and 24%, while funding costs remain much lower, ensuring strong spreads and healthy margins.

Since the loans are secured against gold, a highly liquid commodity, credit losses are minimal, with sector NPAs historically around 1–2%.

Muthoot’s edge lies in its vast distribution network and operational expertise. With more than 7,000 branches, the company enjoys three clear advantages:

- Sourcing density

- Reliable custody of pledged gold

- Local trust that encourages repeat borrowing

Its disciplined operations include consistent evaluation, standardized valuation, secure storage, and well-practised auction processes. These practices convert pledged gold into recoverable value with remarkable efficiency. Replicating such a model across a wide geography is extremely difficult for competitors.

Why the gold rally is a direct earnings lever

Rising gold prices feed profitability through straightforward mechanics:

- Higher price per gram increases absolute loans against the same jewellery, lifting the average ticket size

- Larger tickets boost AUM and interest income without proportional increases in footfall or branch count

- Appreciating collateral increases recovery cushions beneath prevailing LTVs, lowering expected loss severity

- Fixed processing costs spread over larger disbursals improve per-transaction unit economics

In the recent cycle, domestic gold prices approached ₹1.06 lakh per 10 grams, coinciding with rapid expansion in organized gold lending. Muthoot reported significant AUM growth and marked quarterly earnings improvement, reflecting these forces: the branch-led machine converted the same household gold pool into materially larger lending volumes.

Regulatory Amplifiers

Policy changes matter significantly. Adjustments to permissible LTV bands influence how much credit can legally be advanced against given gold stocks. Upward LTV revisions expand borrower access and raise lender disbursal capacity.

Muthoot’s disciplined approach to average LTVs and operational auction control reduces policy friction, translating regulatory tailwinds into actual growth.

Operational disciplines and durability

The recent boost in gold prices is real, but the permanence depends on execution. Key controls sustaining the model include:

- Conservative LTV oversight

- Thorough purity verification

- Secure storage protocols

- Transparent auction procedures

- Proper liquidity management

Lenders relaxing valuation standards to chase market share can quickly convert price rallies into capital illiquidity if the commodities correct.

Market Perspective

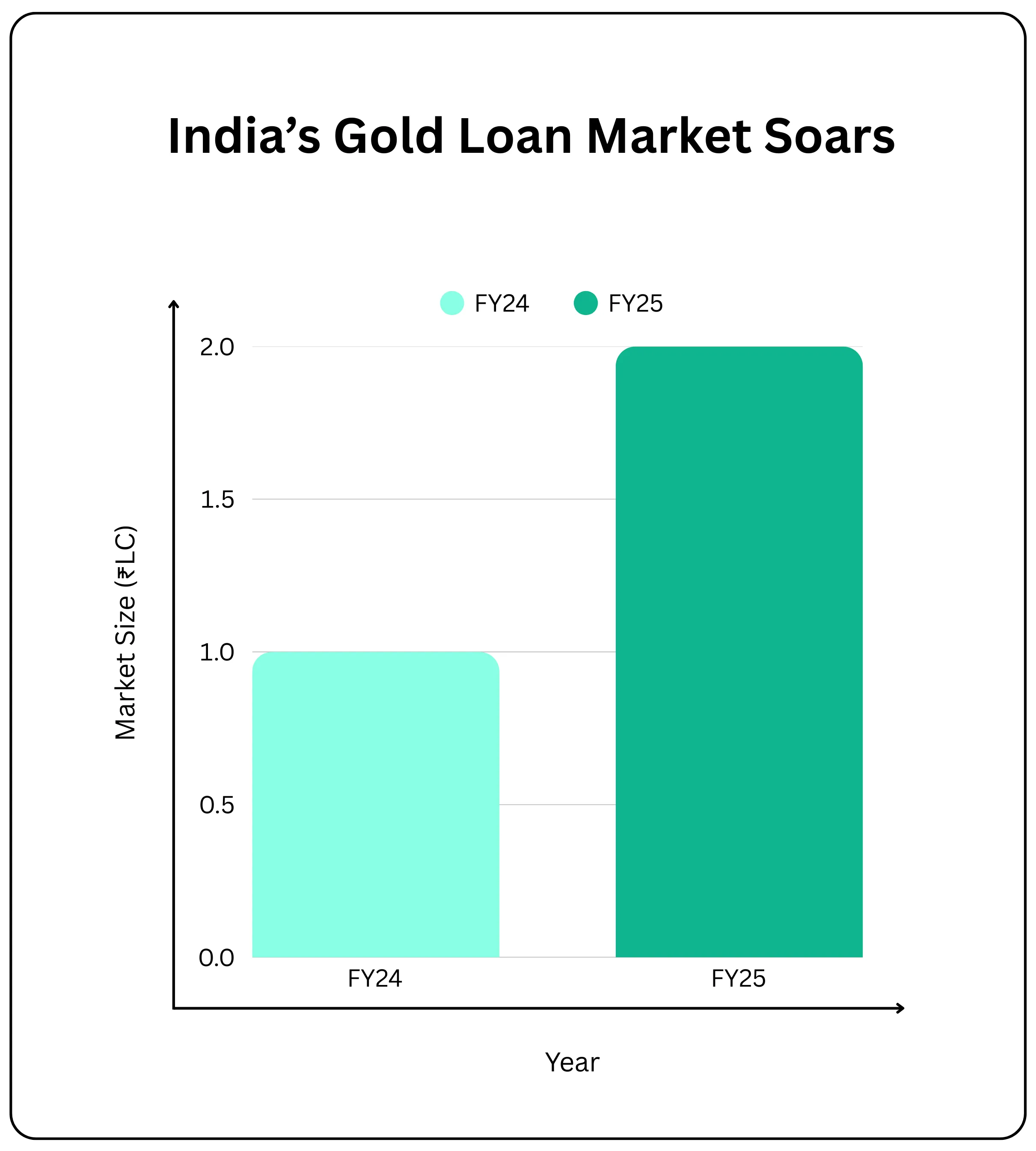

The Indian gold loan market’s 103% growth to ₹2.1 lakh crore reflects accelerating formalization and regulatory support, with forecasts suggesting ₹14.19 lakh crore by 2029.

Muthoot Finance exemplifies this opportunity. 37% AUM growth, rising ticket sizes (₹93,000 average), and robust NIMs of 11.4% demonstrate how gold rallies amplify established models.

Net Interest Margin (NIM) is a key measure of Muthoot Finance’s lending profitability. It shows how efficiently the company turns its funding into earnings — calculated by subtracting interest paid (on debentures and borrowings) from interest earned (mainly on gold loans), and dividing this net income by the average loan book for the year.

For example, in FY25, Muthoot Finance earned about ₹1.69 lakh crore in interest and paid ₹64,000 crore as interest expense, resulting in a net interest income of ₹1.01 lakh crore. With an average loan asset base near ₹9.2 lakh crore, the company’s NIM stood robustly around 11.4%.

This high margin is enabled by their focus on secured, short-tenure loans and a large base of retail debenture investors, who help fund growth at competitive rates. Recent Muthoot Non-Convertible Debentures (NCD) have offered yields in the 8.25–9.3% range. High NIMs give Muthoot a buffer for potential risks and fuel its strong earnings trajectory, even as the competitive landscape evolves.

While competition from banks and gold price volatility pose risks, Muthoot’s operational expertise positions it to capitalize on India’s vast untapped household gold reserves. The company’s centuries-old relationship capital, combined with market tailwinds, supports sustained growth potential.

Disclaimer: The information provided in our blogs is for informational purposes only and should not be construed as financial, investment, or trading advice. Trading and investing in the securities market carries risk. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Copyrighted and original content for your trading and investing needs.

© 2025 — Tradejini. All Rights Reserved.